en

en

da

da

Financial Controlling often focuses primarily on ensuring accurate external annual reporting. While this is both understandable and important, unfortunately, this focus can compromise the quality of internal financial management. In this article, we therefore examine how Financial Controlling can strengthen internal management reporting and contribute to value creation without compromising the quality of the external annual report.

They are typically part of the monthly cycle in most companies: the internal management reports that provide the board of directors, executive management and other business leaders with an overview of the company's financial performance and whether they are on the right track.

Particularly for the board of directors and executive management, who are evaluated by external stakeholders based on the annual and interim reports, there is a focus on understanding and evaluating how the financial figures are developing. And since preparing the annual report is a substantial task, many companies use their internal monthly reports to continuously ensure the foundation for the annual report leading up to the major annual 'examination'.

Therefore, external accounting principles are typically also applied in internal reporting, using the same definitions, calculation methods, formats, layouts etc. This is usually a significant responsibility of the company's financial controller, who is also tasked with ensuring data quality.

However, ongoing internal management reporting serves another significant purpose: to understand and evaluate how the underlying business is developing, enabling intervention in case of unfavorable trends. To succeed with this important task, there is typically a need for something different from and beyond financial statements prepared and presented according to external accounting principles and requirements.

As a reader of financial reports, this is likely neither new nor surprising to you, and we do observe that most companies' internal reporting contains more than just externally prepared figures. However, we have chosen to address this because we see significant potential for improvement in many companies. It is our experience that the external purpose carries far more weight than the internal purpose, resulting in diminished quality of the basis for business-related financial management.

Below, we will therefore provide a number of examples and recommendations that can contribute to value creation by helping business management and their departments better understand financial developments and their underlying causes.

To succeed, it is necessary to examine which figures and data are being monitored, how they are calculated, and how they are presented.

Define relevant KPI's and structures

In addition, we recommend supplementing the reporting with a number of more operational indicators and key figures – preferably so-called leading indicators – to enable quick intervention in response to unfavorable situations or developments.

It goes without saying that the selection of KPIs must be defined and tailored to each individual company, and this will largely depend on the industry. Beyond establishing the relevant data and KPIs, these also need to be structured. This is best achieved by defining and reporting them in relation to the company's management and business model.

It is therefore crucial that the above is defined in close collaboration with business management and individual parts of the company, ensuring that everyone is measured on what they can relate to and influence. Here is a far from exhaustive list of examples of such KPIs:

- Employee, customer and/or supplier satisfaction

- Quality in product, service, production and/or delivery

- Order intake and backlog

- Sales patterns and mix

- Production time and costs

- Runtime

- Sales pipeline

- Sickness/absense.

Be careful with accounting principles and calculation methods

When companies prepare their external annual reports, each accounting item is calculated according to specific standards; in Denmark, this is typically the Danish Financial Statements Act (ÅRL) or the international IFRS standards. The purpose of these calculation methods is to provide readers of financial statements with a clear insight into the company's financial results and position. This also enables comparative analyses between companies that follow the same principles.

The external principles are thus not determined based on a desire for or need for operational financial management. So if internal management reporting is to serve this purpose, it will be necessary to consider calculating some of the significant accounting items differently. Here are some examples:

Contribution margin and inventories

- Accounting rules require the inclusion of IPO (Indirect Production Overhead) in the cost price of inventories. This results in the contribution margin containing shifts in the IPO surcharge.

- Since indirect production costs such as overheads and depreciation do not vary with production volume, it becomes less transparent to understand the development of the reported contribution margin when the company applies this accounting principle.

Research and development (R&D)

- According to IFRS – and ÅRL for larger companies – companies must capitalise both external and internal development costs.

- Since there is typically more focus on the bottom line than on the balance sheet total, there tends to be a strong desire to capitalise as many R&D costs as possible, just as the expensing in the form of subsequent depreciation does not 'burden' the gross profit.

Leasing

- According to IFRS, certain leased assets must be treated as if the company owns the assets in question; i.e., they must be capitalised, depreciated etc.

- This view of leased assets does not always align with the needs of financial management, which can be conducted much more simply by focusing on the lease payments. The choice of leasing as an alternative to purchase is precisely made for business reasons.

In these cases, companies that apply external accounting principles in their internal reporting may find that this can compromise the relevance of ongoing reporting and the quality in terms of conducting financial management.

Not only can the calculation methods be complicated and opaque. Sometimes they can also involve significant estimates. The latter may be due to subjective estimates being included in the calculations, which are sometimes (mis-)used for earnings smoothing. Thus, a lot of time is spent ensuring 'correct' monthly figures in accordance with external principles

From a financial management perspective, however, this does not contribute to understanding the underlying business development or to making optimal business decisions. On the contrary, the analyses become more complex or even meaningless to perform.

The same applies to internal allocation of costs and profit. Here too, there is a risk that external requirements for presenting segment information and compliance with tax legislation ‒ so-called transfer pricing ‒ result in data losing value in relation to internal business financial management.

Choice of presentation format is important for understanding

A third aspect that Financial Controllers and others responsible for internal reporting should consider is how the selected data should be presented. Here too, there are several factors that may differ from external reporting.

Classification

Without changing the accounting principles or values themselves, it may be beneficial to present some of the accounting items differently.

For example, it could make good sense to split net revenue into gross revenue and discounts. This way, you can better monitor how discounts develop over time.

Perhaps the internal reporting could also benefit from a clearer and different separation between variable and fixed costs than what is typically seen in the external income statement.

Tables and graphs

You have probably experienced this before: To keep track of how the company is performing compared to previous results and full-year expectations, monthly and YTD figures are often presented in tables. These tables compare with last year's figures and the budget, showing the variances.

However, there are significant challenges with this approach. Firstly, the tables do not always provide an easy and intuitive picture of the actual development. Secondly, they can lead to a one-sided focus on variances, such as how much we deviate from the budget in a given month. Here, graphs illustrating the development of various key figures over time can be far more useful and valuable.

Comparative figures

Reporting is largely used to evaluate company performance, though there is rarely a single and unambiguous answer to this.

The task is often addressed by comparing accounting figures with last year and with budget. This is a simplified way of evaluating performance and should therefore be done with caution.

It might be worth considering supplementing this method by showing the development of certain key figures without any reference to a monthly target (budget or similar). Simply showing the development over time provides great value, and it will typically lead to good questions and business discussions: Is the development moving in the desired direction? Is the level constant, or are there significant fluctuations and why? Is the level acceptable?

Financial Controlling plays a crucial role

As shown, your company's financial controller plays an important role in developing, implementing and operating the company's monthly reporting. In larger companies, where controller tasks are divided between Financial Controlling (or Accounting & Reporting) and Business Controlling/Partnering (or Business Finance), the design and quality of management reporting will depend on close collaboration between these parts of the finance team.

When companies ‒ as recommended here ‒ choose to supplement their internal management reporting with calculations, KPIs, and analyses that are prepared differently than in the external annual report, there is an extremely important role in bridging the gap between external and internal reporting. Without this reconciliation, uncertainty about the figures may arise, which must be avoided at all costs.

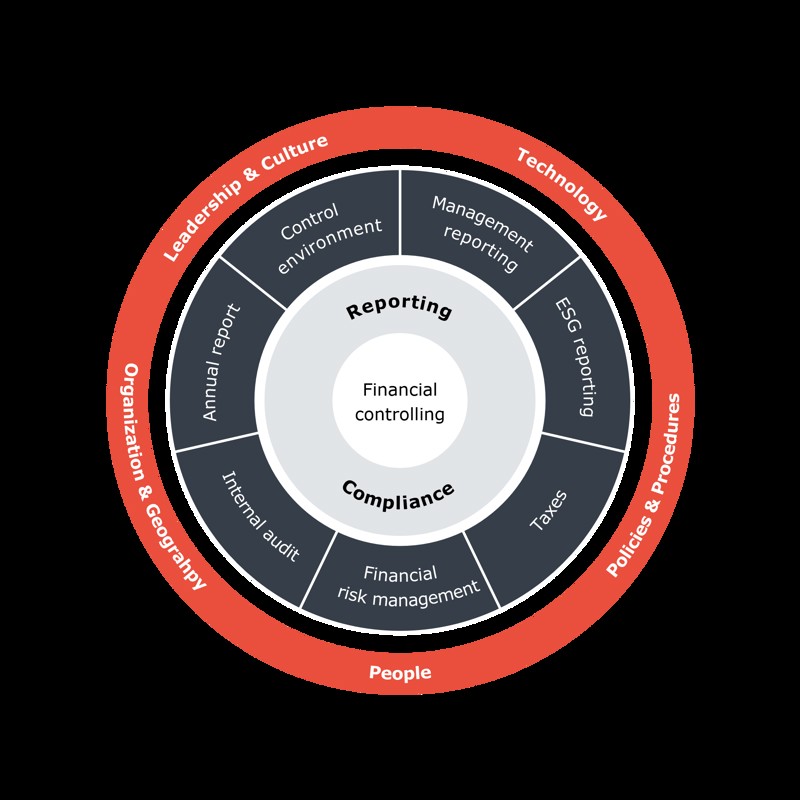

Finally, Financial Controlling has an important role in ensuring instructions, processes, systems etc., which must guarantee satisfactory quality of internal management reporting, cf. our Financial Controlling & Compliance Framework.

The figure illustrates that the foundation of a finance organisation delivering at a high level of quality and efficiency is formed by the interaction between management values and corporate culture, technology support, policies, employees and organisational structure. Furthermore, the figure illustrates the assistance and solid experience that Basico can offer within the 'Finance - Reporting & Compliance' area.

What is your next step?

If you recognise these challenges and would like inspiration or assistance in implementing changes to your company's internal management reporting, please feel free to reach out.