en

en

da

da

Introduction to ESG taxonomy and reporting as well as recommendations for future work

New requirements from investors and the labour market for non-financial data

The largest Danish companies, accounting classes large C and D, have since 2009 been subject to requirements to account for their work with corporate social responsibility, which has most recently been tightened with a legislative amendment in 2018 with effect in 2020 – a general focus on reporting on the company's social responsibility, which is referred to as CSR, an abbreviation for Corporate Social Responsibility.

In 2021, ESG, which stands for Environmental, Social & Governance, was added as a supplement to CSR, but with the specific focus of meeting requirements from investors and analysts for non-financial data regarding companies' historical performance within social responsibility.

The difference between CSR and ESG

CSR covers a broad collection of sustainable activities, for example social conditions, corruption and bribery, human rights and employee relations. CSR thus describes the company's social responsibility and covers everything from climate and environmental considerations to considerations for society in general. CSR aims to accommodate a broader group of stakeholders, e.g. authorities, community organisations, customers and employees.

ESG is an expression of the specific areas regarding non-financial data, which are increasingly being requested by investors and analysts when assessing companies' social responsibility. There is not yet a common global standard for ESG or for which metrics should or ought to be included in the valuation of a company, but the latest directives and regulations, such as Corporate Sustainability Reporting Directive (CSRD), Corporate Sustainability Due Diligence Directive and the EU taxonomy, may set the standard going forward – even though a significant simplification has currently been proposed.

With increased focus on social responsibility and particularly climate impact, CSR – and thereby ESG reporting – has gained greater and greater importance for the external assessment and valuation of companies and is now considered central to companies' business strategy. Furthermore, it has become an assessment parameter and in several cases an entry requirement for investors and lenders.

How companies should relate to ESG in connection with their strategy and reporting is constantly evolving, but some decisive steps have been taken at international level over recent years. This has happened with the establishment of the International Sustainability Standards Board (ISSB) and the publication in 2022 of two standards – IFRS S1 and IFRS S2 – which focus on climate-related information and general sustainability information, respectively.

The tracks are being laid while the train is running

The development in external requirements regarding ESG from both the EU, investors, lenders and employees has happened so quickly that it has not been possible to establish one common standard and practice. This naturally creates a challenge for companies and is also often a very manual and time-consuming process that must be solved by employees who have not yet built up years of experience in the area.

But ESG reporting is here to stay and has increased in scope in recent years. Furthermore, it has gained greater influence on the valuation of companies, access to financing opportunities and the ability to attract employees – which is why it rightly occupies a significant place in companies today.

Environment (E)

When a company is assessed on the environmental area, it is examined how the company treats the environment. In this context, one looks at, among other things, what their energy consumption is, and how much CO2 they emit.

Social matters (S)

Here it is assessed, among other things, how the company ‒ and possibly their suppliers and partners ‒ treats its employees, including whether the company respects fundamental human rights and workers' rights. It can also be taken into consideration whether the company contributes to the local community.

Corporate governance (G)

The company's management is assessed on, for example, whether conflicts of interest exist in the management, the gender composition of the board, and whether the company's accounts are transparent and comprehensible.

If we compare ESG reporting with other external reporting in the annual report, it differs primarily by consisting of non-financial data – but still data nonetheless. It is still information that must be continuously defined, collected, checked, documented, consolidated and reported. The primary difference is often seen in the registration itself, where there is a need to expand the existing process to also include underlying data for calculating the new metrics.

But regardless of whether we are talking about financial or non-financial data, it is advantageous to put it into process to ensure that data is collected stringently, homogeneously and automatically. Furthermore, data, financial or not, requires a clear definition that can both be communicated and formulated – which also makes it easier to continuously calibrate the method when it has already been systematised.

What can you do already now?

Given the uncertainty about both the scope of metrics and calculation methods in combination with a relatively short timeline between potential publication of definitions and reporting requirements, you can benefit from beginning the preparatory exercises already now.

This applies particularly to establishing a real process for collection, handling and reporting of ESG metrics, so you have a starting point when potential changes come knocking. And should they not come, you will have a process that ensures efficient use of your employees' time and brain power.

By establishing a process, it will be possible to ensure:

- That data and documentation are collected continuously in a structured and uniform manner.

- That there are clear guidelines for how data points should specifically be measured and defined.

- That information can be consolidated and added to the existing reporting system and its processes.

Furthermore, it will make it possible to support data collection with systems and allow it to be included in the existing data volume and data flow, where definitions and calculations are managed centrally. In this way, adjustments can be documented and embedded at short notice, as guidelines are published.

ESG is today included in the management report, such that it must be reported in accordance with the same deadlines as the rest of the accounts. This means that the non-financial requirements must be fulfilled in a period that is already characterised by scarcity of hands. Additionally, underlying data are not necessarily easily accessible. Especially not if, as a company, you span across multiple countries. In those cases, it can be advantageous to start the process regarding data collection, principles, validation and documentation in good time – if you have not already begun.

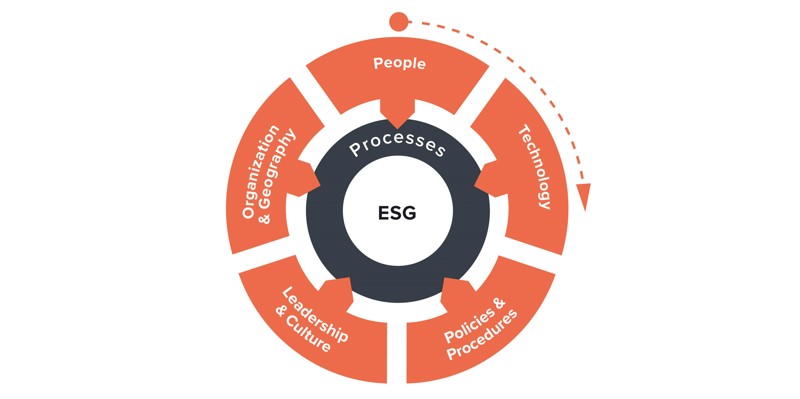

Five focus areas to ensure your process is spot on

When it comes to processes, we typically see that the five areas below must work together for the processes in the finance function to work. You must ensure:

- The right, and sufficient, competencies – either through education or recruitment. The latter can be particularly challenging, as the market for ESG in recent years has been red-hot, and as the supply of employees with the right experience is low compared to demand.

- System support of the process or data collection, consolidation, controls, master data, definitions and calculation as well as reporting.

- Clear internal rules of the game and a definition of how to internally address the increased requirements from external parties, e.g. diversity in recruitment, waste management, CO2 emissions, electricity consumption etc.

- Clarity about what culture (change) is desired on the basis of a new process. Additionally, you must assess whether there is a need for changes to the management structure or finance's role in the company.

- The right organisation. Can the new process be handled by the existing organisation/team, or is there a need to reorganise in relation to where the information is found?

When it comes to processes, the five areas above must work together for the processes in the finance function to work. Basico's resource model can help you focus on precisely these five areas, so your process is spot on.

Do you need help creating a process for your ESG reporting?

At Basico, we have many years of experience with implementation and embedding of new reporting requirements – whether driven by external or internal needs.

Would you like to ensure that you are ahead of the curve with reporting your ESG metrics by establishing a good process for data collection? Then do let us have a conversation based on your company's needs and existing processes.