en

en

da

da

Reflecting on the year-end closing for 2024 – and how these experiences can be used to strengthen Finance going forward to support the next year-end closing – is an obvious and recurring annual exercise. At the same time, it is important that you are aware of changes in the accounting regulations for 2025, so they can be handled in due time.

The calendar says mid-March 2025, and this means that many companies have already completed their annual report and are fully engaged in operational tasks in Finance for the new year – and in a rapid pursuit of projects that must be completed before the summer holidays.

But before the experiences from the annual report process are completely forgotten, you can advantageously consider how any errors, reworks and input from management and your auditor can be used constructively – both to strengthen the 2025 annual report and to improve daily business procedures and internal controls.

This is because the year-end closing process – including the preparation of the annual report itself and its audit – typically involves a much deeper review of the accounting treatment of the company's activities and is therefore an important data point for assessing the quality of processes in Finance.

Finally, it is obvious to use the occasion to look at the general need to update risk understanding, business procedures, internal controls etc., so that risk management follows the company's risk policy, and Finance operates effectively.

To convert improvement potentials from the recently completed year-end closing process, there are, among others, the following obvious measurement points for the year-end closing process that you can dive into to reflect on whether there are important experiences you can benefit from.

- Was the timeline adhered to, and did the task of preparing the annual report and the supporting documentation proceed without surprises? Or were corrections of accounting errors or information in the draft annual report necessary because risks emerged that had not been identified or correctly assessed ‒alternatively that the controls did not prove effective?

- Were everyone's roles and responsibilities well-defined, so no tasks fell between two stools or were solved by multiple people? And did you avoid "backflow" by ensuring your expectations regarding documentation scope and format were aligned in advance?

- Are the people involved still in good spirits? Or has the year-end closing process resulted in an exhausted and perhaps stressed Finance organisation?

- Was management sufficiently informed about the timeline and about when their input and commitment to decisions were necessary – e.g. regarding expectations for the future, estimates and risks? And could the auditor advantageously have been involved earlier to clarify the treatment of any uncertainties or simply to support a more efficient or accelerated year-end closing process?

2024 offered only minor legislative changes. The same is the case for 2025 – for some

As you already know, 2023 offered only a few legislative changes such as:

- Increase of the size thresholds for turnover and balance sheet total (Danish Financial Statements Act) by approximately 25%, which means that certain companies are already subject to fewer disclosure requirements and more lenient accounting policies in selected areas with the 2024 annual report.

- A new Bookkeeping Act with new requirements for a digital bookkeeping system (for certain companies using a non-registered bookkeeping system, however, the requirements for digital bookkeeping will not apply until 2025 – and for personally owned businesses not until 2026). You can read about what this entails – for some it is extensive – in the article here.

- Minor amendments to a number of IFRS standards (IAS 1, IAS 7, IAS 21, IFRS 7 and IFRS 16) following approval in the EU.

For 2025, the changes to financial reporting are very limited, regardless of whether the annual report is prepared according to the Danish Financial Statements Act or IFRS. For the Danish Financial Statements Act (large C), it concerns disclosure of intangible key resources, while for IFRS it concerns currency exchange in special situations. Additional amendments to IFRS await approval in the EU and will not apply until 2026 at the earliest.

Companies belonging to accounting class C (large) should be aware that the requirement for sustainability reporting according to CSRD, CSDDD and the taxonomy applicable from 2025 is now expected to be postponed and eased with the European Commission's Omnibus proposal. The political process is ongoing, which is why the extent of adjustments to the companies covered, the timeline and the reporting requirements for ESG reporting are uncertain.

We have previously published a series of articles targeting ESG, but the timeline and support of the reporting requirements etc. should be read with reservation, taking into account the Omnibus proposal.

The timeless "classics"

Although your company is not affected by the changes to the Danish Financial Statements Act and/or IFRS or directly or indirectly by the ESG requirements, a number of timeless "classics" still apply. This is when your company:

- at management's initiative develops new needs for better business insights for decision-making

- increases or reduces its activities

- makes investments possibly requiring financing or changed capital structure

- needs to be prepared for sale or IPO

- reorganises Finance, for example, for higher quality and efficiency, cost savings or something else.

Do you see the big (risk) picture?

A company can be compared to a living organism – both due to changes in internal factors and the influence from the changing external factors. Therefore, there is a continuous need to look at the risk picture in terms of adjusting and trimming the control environment to mitigate business, reporting and compliance risks.

With the article's focus on the annual report process, the delimitation is at the entity level, but the control system must embrace the risks, regardless of which "interface" is applied, e.g., for internal management purposes.

We have published a series of articles specifically targeting identification of risk assessment and implementation of appropriate internal controls, which you can read more about here.

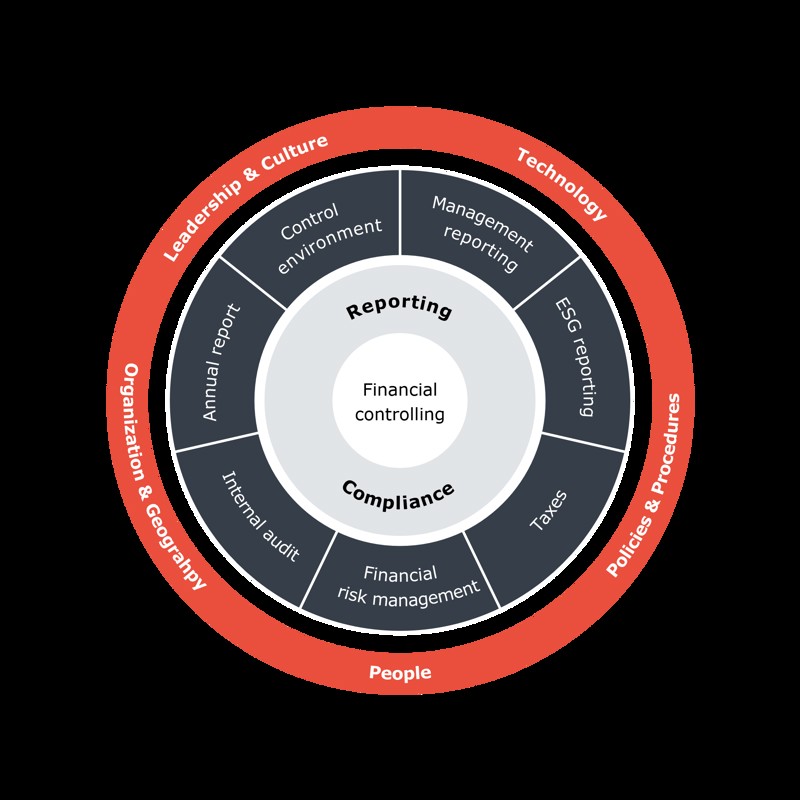

The figure illustrates that Financial Controlling is the foundation for the finance function's areas of responsibility: Reporting and Compliance, which consist of a series of core tasks. To achieve a high level of quality and efficiency, these must be adapted to the company's specific circumstances and the framework conditions, which you can see in the outer ring of the circle.

Basico can contribute with advice and assistance within all areas of the model.

Can we help?

With us, you receive specialised help with everything from annual reporting – whether your company is listed and subject to IFRS or follows the Danish Financial Statements Act – to sustainability reporting and improvement of risk management, e.g. in the form of internal controls. We help you strengthen the foundation of your finance function, allowing you to spend fewer resources on firefighting and more on creating progress.

Do you need sparring, or would you like to hear more about how we can support your business? Then reach out to Mikkel Harloff-Helleberg, Partner in CFO Services.