en

en

da

da

From ordering to payment. These are, in broad terms, the processes that PtP covers. While it may sound simple, there are potentially many pitfalls in these processes, precisely because multiple organisational areas and systems are often involved.

This is why well-optimised and efficient PtP processes can make a significant positive difference. However, it also requires balancing robust compliance with effective execution. In this article, we guide you through the process from policies to practice: First, we define the necessary policies, then we look at the design of PtP processes and approval hierarchies, and finally, how it all comes together in a risk matrix tailored to your company's needs.

The foundation for an effective PtP process: from policy to practice

In this section, we take a closer look at the foundation of well-functioning PtP processes. Before diving into the specific processes and approval hierarchies, it is essential to understand the connection between policies and processes, as this hierarchy forms the basis for an effective process chain and is therefore a prerequisite for successful implementation.

Effective PtP processes are built on clear policies that define the framework within which the processes should be designed. These policies can be more or less extensive and detailed depending on the need and typically include:

- Procurement policy: Establishes the overall framework for the company’s procurement activities, including whether the procurement function should be centralised or decentralised. The policy also defines which types of purchases require prior approval and how different procurement categories should be handled differently – for example, differentiated requirements for purchasing production equipment versus regular operational purchases.

- Authority policy: Defines who is authorised to enter into agreements and approve transactions on behalf of the company. This includes spending limits, approval levels and any specific requirements for certain types of purchases. The policy is fundamental to the company’s risk management through internal controls.

- Supplier policy: Sets the framework for how the company selects, evaluates and collaborates with suppliers. This includes criteria for supplier approval, documentation requirements, ethical guidelines, and how supplier relationships should be maintained. The policy may also include requirements for suppliers’ sustainability profiles and compliance.

- Segregation of duties policy: Ensures that critical tasks within the PtP processes are not performed by the same individual. This is a key element of the company’s internal controls and includes, for example, the separation of ordering, approval and payment. The policy is crucial for preventing errors and fraud.

- Working capital objectives: Defines the company’s strategy for liquidity management, including payment terms, credit periods and inventory management. This policy is central to optimising the company’s cash flow and has a direct impact on how procurement and payments should be structured.

- Technical policy: Defines the framework for system integration and IT security within the PtP process. This includes managing user access rights, requirements for system integrations between the ERP system and other IT systems as well as the potential implementation of e-procurement solutions. The policy ensures that technology supports the processes effectively and securely.

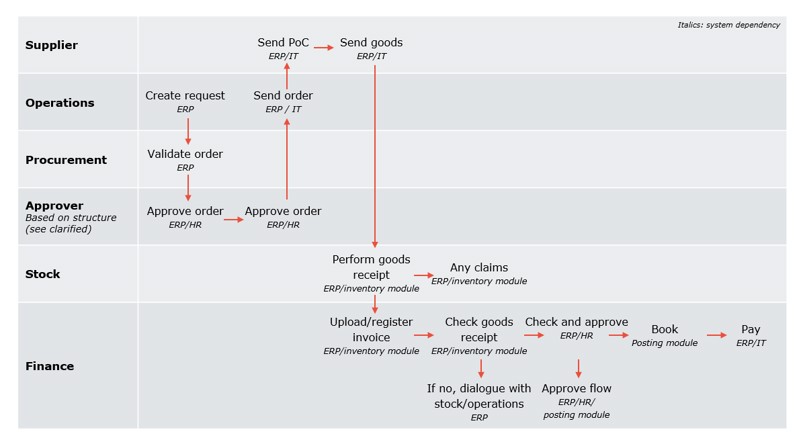

With the policies defined, we now have the foundation in place to design effective processes. The policies set the framework, but the real value lies in how we translate them into practical workflows. Let’s therefore take a closer look at the process chain (the processes from A to Z), which represents the concrete flow from the emergence of a procurement need to the completion of payment.

The figure illustrates the complexity of the process chain, including the involved employees, departments and systems as well as the extensive communication.

As the process chain shows, the policies manifest differently throughout the flow. The procurement policy governs the initial phases, the authority policy defines the approval flow, while the working capital policy particularly influences the final stages of the chain. At the same time, the technical policy ensures that the entire flow is effectively supported by the company’s systems. Successful implementation, therefore, requires not only an understanding of the individual policies but also how they interact throughout the entire process chain.

The process chain is typically integrated into the company’s ERP system, but the complexity increases due to the many organisational layers and potential system integrations. This places specific demands on process design and attention to dependencies ‒ both in terms of automation opportunities and risk management.

With this foundation in place ‒ from policies to organisation ‒ we can now focus on designing the specific approval rules and hierarchies that will ensure the effective implementation of the policies in practice.

How do we design the approval rules?

The approval rules are where the authority policy meets practical reality. The three approval levels we will now examine are the concrete implementation of the company’s established policies for segregation of duties, risk management and operational efficiency. It is about precisely defining which employees or roles – and how many – are involved at which stages, as well as determining the approval levels to be assigned according to the company’s authority rules.

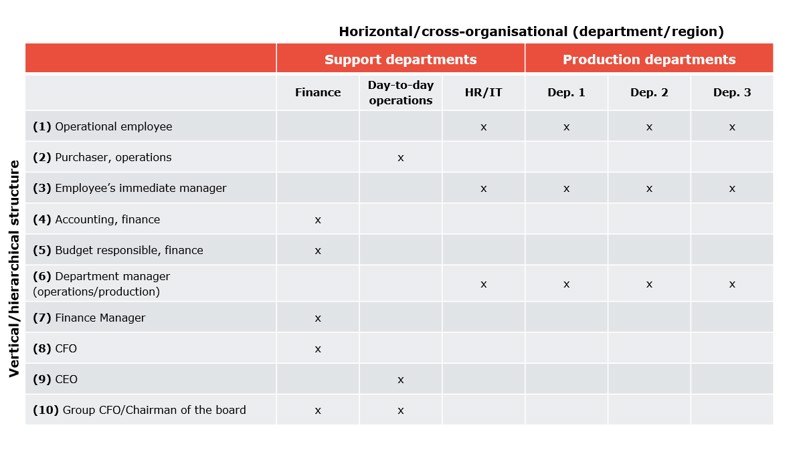

Potentially involved employees in the approval flow

Effective approval rules require a clear division of roles and responsibilities across the organisation. The table below illustrates how different levels in the hierarchy can potentially be involved in the approval process.

-

First Level (rows 1-4 in the table)

Includes buyers and operational employees. In large companies with formalised and mature procurement processes, the primary focus is on goods receipt and performing a three-way match between the invoice, purchase order and inventory. In smaller companies, or for ad hoc purchases without formal purchase orders, the invoice is checked against the received goods/services and the agreed terms. This level ensures that the basis for subsequent invoice approval is accurate. -

Second level (rows 5-7)

Typically includes budget holders or middle managers who, due to their position, are authorised to approve transactions within the established spending limits. This level represents the first actual approval step in the process and is responsible for approvals within their respective areas, including ensuring compliance with the area's budget. -

Third level (rows 8-10)

Includes the chain of management above the budget holders, typically senior management up to the board of directors. This level is only activated for amounts exceeding what budget holders are authorised to approve and is differentiated so that the frequency of approvals decreases as hierarchy levels rise. For example, only transactions related to acquisitions, large financing frameworks etc. may require approval from the board chairman. However, there may also be expense types that receive significant attention (e.g., for risk or cost-saving reasons) and must be approved by senior management, even if the amounts could technically be approved by individuals at levels 5-7.

The number of individuals involved in the approval processes must be carefully considered, balancing resource consumption and approval speed against risk. A well-defined cost center structure and setup are essential to ensure that the right individuals from both support and production departments participate at appropriate levels without overloading the process with unnecessary involvement of multiple parties at the same level. This helps maintain an efficient and focused approval structure.

At the same time, the need for continuous approval of smaller transactions, such as fees, office supplies and recurring subscriptions, can often be determined relatively easily. In such cases, it may be relevant to design exceptions to the approval requirements. Essentially, this is about finding the right balance between risk and resource consumption.

An approved purchase order serves as the framework for the subsequent process and should not require renewed approval at the invoice and payment stages, as long as the invoice matches the order within acceptable tolerances (e.g. +/- 5%). Only in cases of significant deviations from the original purchase order or particularly critical transactions should new approval be required. This ensures efficient processes where the original approval of the purchase order is respected as the governing framework for the entire transaction.

Risk matrix as a management tool: adapting to the company's characteristics

Process policies, the process chain and considerations of approval hierarchies and rules come together in a risk matrix, which serves as the central tool to ensure that policies are followed in practice. The matrix maps out how each policy is implemented through specific controls and how these controls are distributed among the various actors in the process chain. This provides management with a comprehensive overview of how policies are operationalised and how risks are managed across the organisation.

The risk matrix for the distribution of employee responsibilities must be flexible and tailored to the size and characteristics of your company, particularly in terms of scale and complexity. A large organisation with activities in different regions will typically require a more complex structure with centralised procurement processes and extensive system integration. In such cases, dedicated roles with clearly defined responsibilities, stringent approval hierarchies and formalised processes are often necessary to ensure consistency across the organisation. Conversely, larger companies operating under a well-defined authority policy may, in some cases, design PtP processes based on decentralised organisation and local decision-making authority.

In smaller companies, overlapping responsibilities are often seen, where the same employee handles multiple functions ‒ for example, both procurement and bookkeeping. Similarly, employees may have broader responsibilities and greater flexibility to cover for one another. For instance, an accounting manager may have broader authority to approve regular operational expenses on behalf of the business, while decisions exceeding set financial thresholds or special situations, such as urgent matters or disputes, are always escalated to CFO or CEO level. This requires particular attention to segregation of duties and the implementation of compensating controls in the approval processes.

A critical design principle is understanding the company’s primary transaction patterns. For example, a manufacturing company with high volumes of material purchases will require different processes than a consulting firm that primarily handles services, travel reimbursements and time tracking. This business understanding is fundamental to designing a process that effectively supports the company’s actual needs rather than simply implementing a standard template.

These design choices are essential to ensuring a process that provides management with the necessary oversight while effectively supporting the company’s operational goals.

The right approach to optimisation

A structured approach to optimising your PtP processes is essential to identify and eliminate sources of inefficiency. By following these steps, you can create a framework for identifying areas with optimisation potential:

-

Understanding the problem (symptoms): Define the specific goals for optimisation in collaboration with the relevant stakeholders within the organisation.

-

Analysing the symptoms: Key personnel from your organisation conduct a detailed mapping of the current approval processes and identify the root causes of issues.

-

Adjust the process chain: Eliminate the identified causes of inefficiency and sources of error.

-

Implementation and evaluation: The solution is initially tested in limited pilot projects, which are evaluated and, if necessary, adjusted before full implementation.

-

Evaluation and redesign: After implementation, results are assessed, and necessary adjustments are made to achieve the desired outcome.

By adopting this approach to workflow optimisation, you can achieve significant improvements in the quality of your company’s PtP processes, while also ensuring both team-wide quality and a seamless technical infrastructure. Your finance department will experience markedly improved performance, efficiency and employee satisfaction. Additionally, it can strengthen your negotiation positions with suppliers if the process previously caused delays in approvals or timelines that weakened the opportunity for better terms.

Shall we help you with your PtP processes?

Reach out for a non-obligation discussion about your PtP processes.